The Rollback Wave

Six Coordinated Administrative Actions That Cleared the Path for Unprecedented Extraction

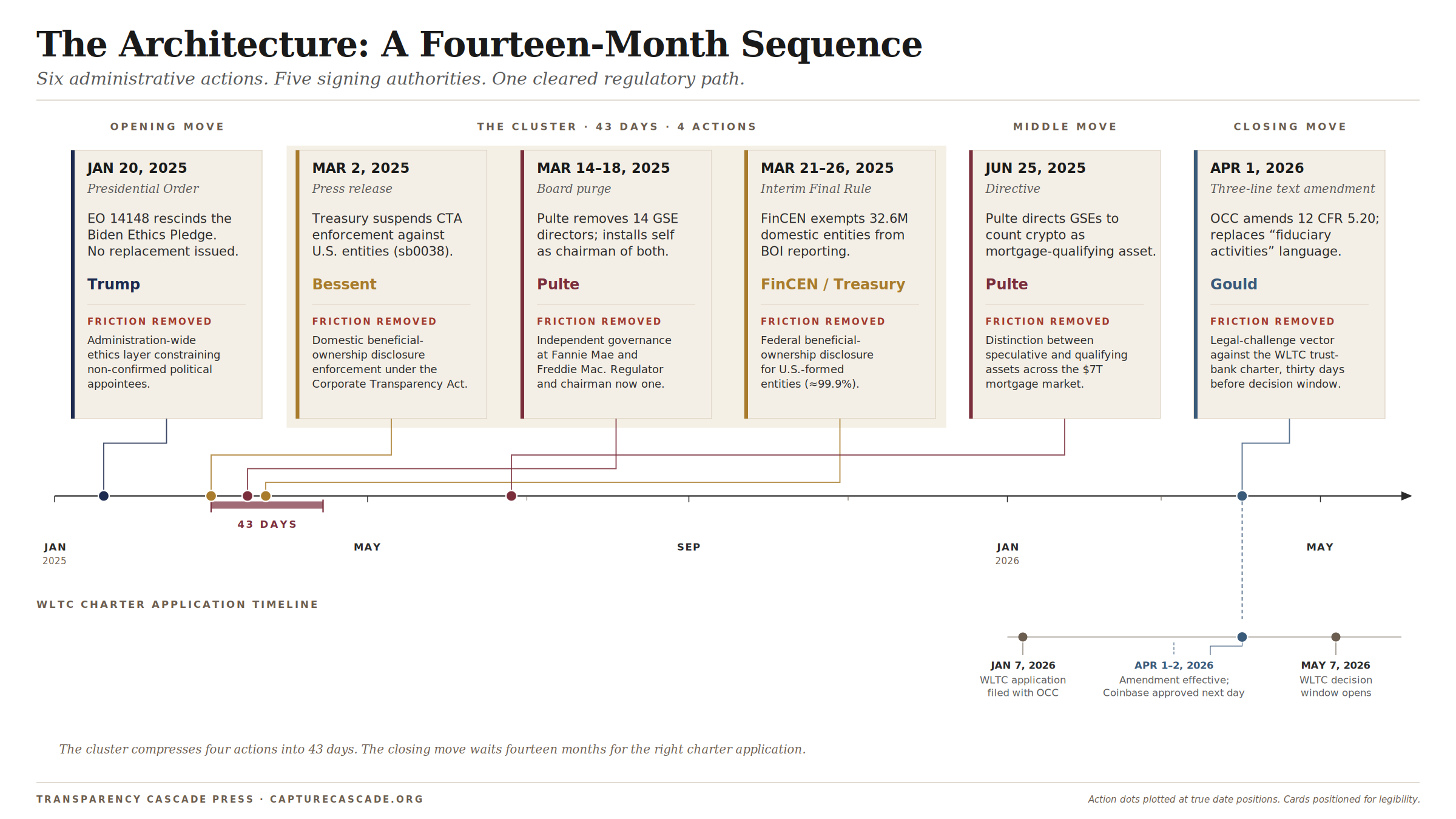

On April 1, 2026, the Office of the Comptroller of the Currency (OCC) published a final rule amending three lines in the Code of Federal Regulations (CFR). Federal Register 91 FR 9977 changed the language governing national trust bank charters, replacing “fiduciary activities” with “the operations of a trust company and activities related thereto.”

Approximately 36 days later, the preliminary-decision window opened for a pending OCC charter application: World Liberty Trust Company (WLTC), the only crypto-native national trust bank application in the queue-- and it’s owned by the president’s family.

The amendment looked routine. Regulatory language-cleanup aligning the CFR to the underlying statute. Comptroller Jonathan Gould signed it. It took effect on April Fools’ Day.

It was not routine. It was the closing move on a six-action sequence that began 14 months earlier, on the first day of the second Trump administration. Taken in full and the pattern is unmistakable: six discrete administrative actions, no new legislation required, each removing a specific oversight or disclosure trigger that would otherwise generate friction against the Trump family’s financial architecture.

The sequence does not look like a coincidence when you see all six actions laid out together.

This is the architecture.

The Closing Move: April 1, 2026

Start with the OCC 12 CFR 5.20 amendment because it is the most recent and the most legible in hindsight.

The amendment’s technical function was to remove a specific legal-challenge vector. Community advocacy groups — the National Community Reinvestment Coalition and Americans for Financial Reform Education Fund — had filed comment letters in February 2026 arguing that World Liberty Trust Company’s planned activities (issuing, redeeming, and custodying the USD1 stablecoin) did not constitute “fiduciary activities” under the pre-amendment text of 12 CFR 5.20. Their argument was a live statutory challenge: if stablecoin issuance is not a fiduciary activity, WLTC cannot use the fiduciary-activity chartering track to become a federally chartered trust bank.

The April 1 amendment eliminated that argument by replacing the potentially ambiguous term — without requiring OCC to win the substantive debate.

The WLTC application had arrived at the Office of the Comptroller of the Currency on January 7, 2026. It took effect on April 1, 2026. The decision window opened on approximately May 7, 2026.

One day after the amendment took effect, the OCC issued a conditional trust-bank approval to Coinbase. This was the first to issue under the cleaned regulatory text. The amended framework was in production use before the WLTC clock ran out.

This is what a carefully sequenced regulatory clearance looks like.

The Cluster: Six Weeks in Early 2025

Walk backward fourteen months. To understand the April 2026 closing move, you need to see what was built during a six-week period that most Americans missed entirely:

March 2 through April 14, 2025 — forty-three days from the Treasury press release that gutted Corporate Transparency Act (CTA) enforcement to the appointment of Don Jr.’s business partner to the Fannie Mae board.

The timeline:

March 2, 2025: Treasury Secretary Scott Bessent announced suspension of the Corporate Transparency Act enforcement. Treasury press release sb0038 suspended enforcement against U.S. citizens and domestic reporting companies, committing to a forthcoming rule change that would narrow the CTA’s scope to foreign entities only. No court order compelled this. It was a pure policy election. The Biden-era bipartisan law requiring disclosure of who actually owns shell companies — a law with a ten-year congressional gestation — had been operative for less than two months. Bessent made it unenforceable in a press release.

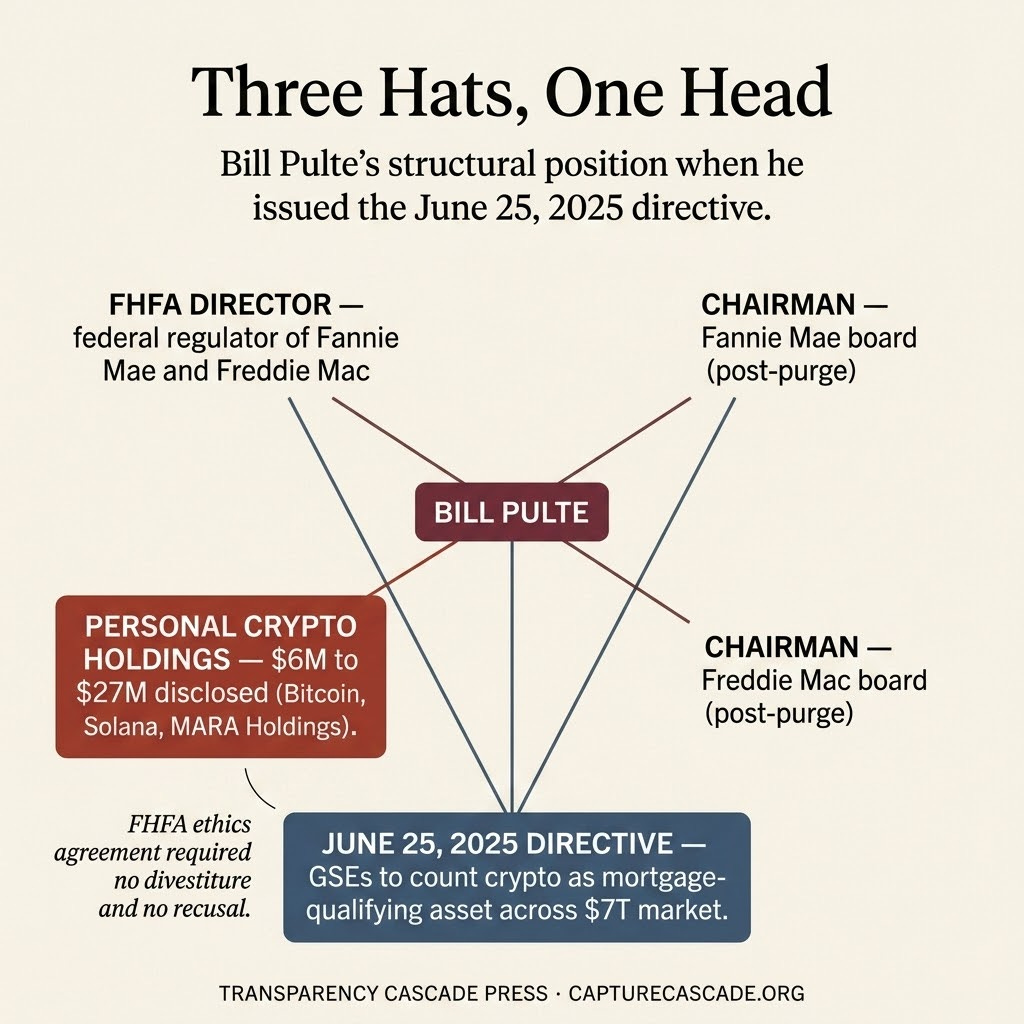

March 14-18, 2025: William “Bill” Pulte is sworn in as Director of the Federal Housing Finance Agency on March 14. Within 72 hours, he removes 14 independent directors from Fannie Mae and Freddie Mac and installs himself as Chairman of both boards — while simultaneously serving as their federal regulator.

The Housing and Economic Recovery Act of 2008 was structured on the assumption that the regulator and the regulated entity’s board would be separate. Pulte made them the same person. Out went a Nobel laureate, a Georgetown securities-regulation scholar, and senior alumni of BlackRock, Morgan Stanley, and the Ford Foundation. The Washington Post reported on the purge the following day.

March 21-26, 2025: The Financial Crimes Enforcement Network (FinCEN) publishes an interim final rule (IFR) redefining “reporting company” under the Corporate Transparency Act to cover only entities formed under foreign law. All U.S.-formed entities — approximately 32.6 million of them, including the Delaware LLCs, Wyoming LLCs, and Nevada LLCs that form the principal vehicles of the Trump family’s deal flow — are permanently exempted from any federal beneficial-ownership disclosure requirement.

The pre-IFR rule covered roughly 32.6 million entities; the post-IFR rule covers approximately 20,000. That is one entity for every ten Americans, dropped from federal beneficial-ownership disclosure overnight. The IFR took effect without a public-comment period, using the regulatory “good cause” exception. Senators Whitehouse and Grassley sent a letter calling it a violation of congressional intent. The rule remains operative.

April 14, 2025: Pulte appoints Omeed Malik to the Fannie Mae board. Malik is the founder of 1789 Capital and Don Jr.’s business partner. The board that now governs Fannie Mae — a $4 trillion institution backstopping the American mortgage market — includes the federal regulator-turned-chairman and his own business associates.

Four actions. Six weeks. Treasury, the nation’s shell-company disclosure regime, the independent boards of the two entities that underwrite the American mortgage market, and the governance of those entities following the purge. Each action targets a distinct disclosure or oversight mechanism. None of them requires Congress. Each uses the least-visible available administrative mechanism.

The Opening Move: January 20, 2025

Back up further still. To the first hours of the second Trump administration.

Executive Order 14148, signed on January 20, 2025, rescinded 78 Biden-era executive orders and memoranda. Buried in that list was Executive Order 13989 — the Biden Ethics Pledge.

What EO 13989 had done was impose administration-wide restrictions on executive branch personnel: a gift-from-lobbyist ban, a two-year cooling-off before joining firms lobbying one’s former agency, a one-year shadow-lobbying bar. These were the structural constraints that prevented non-Senate-confirmed political appointees — the people staffing middle tiers of Health and Human Services (HHS), Federal Housing Finance Agency (FHFA), the OCC, the agencies whose rulemaking most directly affected Trump-family holdings — from operating without any ethics guardrail.

The Hill reported the same day on the rescission. The rescission was news for approximately twelve hours.

Here is what made it architecturally significant: no replacement ethics pledge was issued. The Obama administration had issued EO 13490 on its second day in office with additive ethics requirements. Trump’s first administration issued EO 13770 on January 28, 2017 — its own ethics pledge, which Trump revoked on his last day as a parting gift to departing staffers. Biden reinstated the ethics structure with EO 13989 on his first day.

The second Trump administration rescinded EO 13989 on day one and issued nothing in its place. General appointees entering federal service were governed only by the statutory default — the minimum the law requires.

The administration-wide ethics layer that had existed across four consecutive administrations, additive for Obama and Biden and present even under Trump 1, was gone.

Before any of the five signing authorities on the six-action sequence was sworn in, the ethics-pledge architecture that would have constrained them was dismantled.

The Middle: June 25, 2025

Between the six-week cluster described above and the April 2026 closing move, there was one more action, and it is the most viscerally legible of the six: the June 25, 2025 Pulte directive.

Bill Pulte — the man who purged 14 independent directors from Fannie Mae and Freddie Mac and installed himself as chairman of both — issued a directive ordering the GSEs to develop proposals allowing cryptocurrency held on U.S.-regulated exchanges to count as an asset for mortgage qualification, without mandatory conversion to U.S. dollars.

No Congressional authorization. No independent board deliberation — those directors had been removed three months earlier. No traditional risk-management review made public. The directive was issued by the federal regulator who was also the chairman of the boards being directed.

At the time of the directive, Pulte’s Office of Government Ethics disclosure showed Bitcoin holdings of $500,000–$1 million, Solana holdings of $500,000–$1 million, and MARA Holdings — a Bitcoin mining company — of $5 million to $25 million. Total disclosed crypto-sector exposure: $6 million to $27 million. His FHFA ethics agreement, signed by the agency’s Designated Agency Ethics Official before he was sworn in, required no divestiture and no recusal from crypto-related rulemaking. The June 25 directive is exactly the kind of rulemaking that would have triggered recusal under any prior administration’s operative ethics pledge.

Fannie Mae and Freddie Mac together backstop approximately $7 trillion in U.S. mortgage credit. A change to what counts as a qualifying asset in their underwriting guidelines is not a technical adjustment; it is a redefinition of what assets the mortgage system treats as wealth.

The directive converts every crypto holding in the Trump-adjacent financial architecture from a niche speculative asset into mortgage-qualifying wealth across the approximately $7 trillion Fannie and Freddie mortgage markets.

That is not a metaphor. Every Bitcoin, Ether, and Solana holder gets a marginal upward repricing the moment the GSEs implement the directive. The FHFA Director who issued the directive is among those holders. The president whose family operates World Liberty Financial — the venture whose dollar-pegged stablecoin USD1 is the capital pipe for the Tahnoon-G42-MGX infrastructure — is among those holders. The structural beneficiaries are precisely the architecture this six-action sequence has cleared the way for.

Fox Business reported the directive the day it was issued, the American Prospect analyzed it in August 2025, and NPR examined the Fannie/Freddie privatization implications in February 2026. The crypto-market reaction generated more column inches than the ethics problem. The architectural significance — that an asset class with concentrated political ownership had just been upgraded to mortgage collateral by the regulator who held it — got the fewest column inches of all.

What Obama, Trump 1, and Biden Did Instead

The comparative-absence argument is where the pattern becomes analytically distinct — not just consequential, but historically singular.

Each prior administration with regulatory authority over financial markets used executive authority.

Obama’s first added: EO 13490 on day two imposed ethics commitments, and the regulatory footprint pointed toward construction — Dodd-Frank, the CFPB, FATCA.

Trump 1 issued its own ethics pledge (EO 13770) and rolled back substantial rules — Clean Power Plan, WOTUS, the DOL fiduciary rule — but the pattern was topically broad rather than architecture-targeted; and critically, the Corporate Transparency Act did not yet exist for Trump 1 to dismantle (it was enacted January 2021 over Trump’s veto, via the FY2021 National Defense Authorization Act).

Biden issued EO 13989 on day one — the very order Trump 2 rescinded. His administration also made other significant executive orders:

additive: BOI rule implementation, SEC climate-disclosure rule, FinCEN investment-adviser AML rule.

rollbacks: Trump 1 orders on immigration, climate, and labor.

The distinctive feature of the 2025 pattern is not its scale. Trump 1 rolled back more regulations in aggregate. The distinctive feature is the targeting: six actions, within fourteen months, each removing a specific friction surface aligned to a specific Trump-family architecture component, executed by five signing authorities (Trump, Bessent, Pulte, Gould, and the FHFA Designated Agency Ethics Official who approved Pulte’s no-divestiture ethics agreement), all via administrative mechanisms specifically insulated from Congressional check.

No prior administration ran a sequenced set of administrative actions — no new legislation, minimally-visible mechanisms, compressed window — each targeting an oversight trigger aligned to the sitting president’s personal financial holdings. In part this is because no prior president’s personal holdings included an active crypto venture, a pending federal bank charter application, and a network of offshore-adjacent shell companies requiring opacity all at the same time.

No Congressional vote was required for any of the six. Congress did not assent to the suspension of CTA enforcement. Congress did not vote to exempt 32.6 million domestic entities from beneficial-ownership disclosure. Congress did not authorize the FHFA director to govern the boards of Fannie Mae and Freddie Mac simultaneously from both the regulatory and governance seats. Congress did not pass the OCC chartering-language amendment.

The template is not just rollback. It is rollback via administrative mechanisms chosen precisely because they are immune to Congressional intervention.

The Operational Template — and What Comes Next

Read the six actions column-wise rather than row-wise and the template becomes visible:

Identify each federal trigger that generates reporting, oversight, or enforcement friction against a specific component of the Trump-family financial architecture. Neutralize each trigger via the least-visible available administrative mechanism — a press release, an interim final rule, a board purge, a directive, a three-line text amendment, a presidential order. Let legislation intervene only if the president signs it.

This template is not a one-time event. It is iterable.

The ethics-pledge architecture built across four consecutive administrations — Obama, Trump 1, Biden — was eliminated in one day. The CTA, a bipartisan statute with a ten-year congressional gestation, was effectively repealed in under four months via an interim final rule using the good-cause exception to bypass notice-and-comment. The independent GSE boards constructed across 17 years of post-HERA conservatorship were removed in 72 hours by a single agency director. The OCC chartering-language ambiguity that advocacy groups had identified as a viable legal-challenge vector was cleared in a final rule published thirty days before the relevant charter decision window opened.

Each precedent demonstrates that what appears durable is administrative, and what is administrative is capturable.

The next-generation move in this sequence is already visible in outline: state-level disclosure regimes. With federal beneficial-ownership disclosure neutralized, the residual oversight layer is now state. New York’s LLC Transparency Act — effective January 1, 2026 — is the lead policy battleground, with an important caveat about its current reach.

New York Governor Kathy Hochul’s December 19, 2025 veto of the expansion bill (S7589-A) limited the Act’s scope to foreign-formed (non-US) LLCs only. US-formed Delaware, Wyoming, and Nevada LLCs — the principal vehicles in the Trump-family domestic corporate map — are explicitly exempt under the Act as currently enacted. That veto is the tell. The politically live question is not whether the NY LLC Transparency Act covers US-formed LLCs today — it does not. The question is whether future state legislation will restore that broader scope, and whether the operational template will move to preempt it before it can.

Delaware’s proposed beneficial-ownership disclosure and California’s corporate-climate-disclosure law are the secondary fronts where that same fight is developing. Expect the operational template to adapt: federal preemption claims against state disclosure registries, federal-court challenges to state beneficial-ownership requirements, and potential federal rules explicitly preempting state-level corporate-transparency regimes. The next frontier is preventing state disclosure from filling the federal vacuum.

The template is demonstrated through April 2026. It is not complete.

The Decision Window Is Open

On approximately May 7, 2026 — 120 days from the January 7 filing — the preliminary-decision window opened for the WLTC Holdings OCC trust-charter application. As of May 12, 2026, the OCC has not issued a preliminary approval.

World Liberty Trust Company would issue, redeem, custody, and convert the USD1 stablecoin — the capital pipe for the $2 billion Tahnoon-UAE-Binance deal, the $500 million Aryam Investment stake, and the Abu Dhabi sovereign fund counterparty infrastructure that has channeled foreign capital into the Trump family’s crypto architecture.

When Comptroller Gould appeared before the Senate Banking Committee on February 26, 2026, Senator Warren pressed him on whether the WLTC application discloses the Aryam/G42 stake under OCC’s 10%-threshold disclosure rule — a stake reported at approximately 49%, well above the threshold the regulation triggers. Gould declined to confirm. The companion piece The Precedent Corridor treats this disclosure gap in detail as the load-bearing APA challenge vector.

Whether or not WLTC receives a conditional approval in the coming days or weeks, the regulatory track was built. That is what the six-action sequence accomplished: not a guaranteed outcome, but a cleared path. The legal-challenge vectors that advocacy groups had identified were addressed before the decision arrived. The independent boards that would have deliberated on the implications of a Trump-family stablecoin custodian were gone before the directive expanding crypto’s role in the mortgage market was issued. The ethics-pledge layer that would have constrained the officials making these decisions was removed before those officials were sworn in.

The question is not whether the Comptroller will issue a conditional approval. The question is what kind of system produces a regulatory environment in which that decision is now the only remaining obstacle.

A companion piece — The Precedent Corridor: How the OCC Built a Trust-Charter Track for the President’s Family — traces the eight conditional crypto-trust charter approvals the OCC issued between December 2025 and February 2026, the ninth (Coinbase) approved one day after the April 1 amendment took effect, and the disclosure-gap analysis from the February 26 Senate Banking hearing that constitutes the load-bearing APA challenge vector.

That piece will ship tomorrow subscribe for free to get that piece.

The RAMM documents the connections that beat reporting can’t see:

4,776+ sourced events at capturecascade.org.

1,988 Counties with signals of potential detention center expansion (Federal contracts, 287(g), real estate traces, etc) at detention-pipeline.transparencycascade.org my site that tracks signals of potential cooperation with ICE and Border Patrol.

129 Community fights over detention capacity built out tracked.

All of this is self-funded, and paid subscriptions are the only way I can continue to do this long term.

Sources

Primary Timeline Events (capturecascade.org):

FinCEN IFR Exempts U.S. Entities from BOI Reporting — March 21, 2025

Trump Administration Moves to Count Crypto as Federal Mortgage Asset — June 25, 2025

Regulatory Primary Sources:

Executive Order 14148: Initial Rescissions of Harmful Executive Orders and Actions (White House, January 20, 2025)

Treasury Press Release sb0038 — CTA Suspension (Treasury, March 2, 2025)

FinCEN Interim Final Rule — 31 CFR Part 1010 (Federal Register, March 26, 2025)

OCC National Bank Chartering Final Rule — 91 FR 9977 (OCC / Federal Register, March 2, 2026)

OCC Bulletin 2026-4: National Bank Chartering: Final Rule (OCC, February 27, 2026; Federal Register publication March 2, 2026)

FHFA Leadership Page — William J. Pulte (FHFA, March 14, 2025)

Reporting:

Trump Axes Biden-Era Ethics Order, Lobbying Restrictions (The Hill, January 20, 2025)

Fannie Mae, Freddie Mac Boards Overhauled by Pulte FHFA (Washington Post, March 18, 2025)

Whitehouse, Grassley Demand Explanation of Treasury’s CTA Suspension (Senator Whitehouse, March 10, 2025)

Whitehouse, Grassley Urge Treasury to Scrap New CTA Rule (Senator Whitehouse, May 27, 2025)

FHFA Directs Fannie Mae, Freddie Mac to Consider Cryptocurrency as Mortgage Assets (Fox Business, June 25, 2025)

Injecting Crypto Into the Mortgage Market (American Prospect, August 28, 2025)

Privatizing Fannie Mae is Risky. Would it be a Win for Taxpayers or Trump’s Donors? (NPR, February 3, 2026)

Coinbase Receives Conditional OCC Approval for National Trust Bank Charter (American Banker, April 2, 2026)